Now that we’ve covered the absolute basics of investing in this blog and I’ve already reported on my own approach to keeping my nest egg safe, I’m going to disclose my long-term investments as well.

Overall, I run two strategies that are regularly populated on a monthly basis via simple savings plans. One is for my later retirement and is based solely on broadly diversified ETFs and ETCs, while the other runs under the name “early retirement” and is intended to pursue the same goal. Not only do I want to secure myself for retirement, but I want to enable myself to do so earlier. I want to reach financial freedom status as soon as possible and be able to pay my monthly fixed costs for rent, insurance and groceries through my investments so that I no longer have to rely on an employer or even the government.

My retirement strategy is based on the well-known world portfolio and thus invests broadly in the stock market, but also in commodities, bonds and real estate. Here, however, I do not fall back on the ARERO world fund, which I always recommend to beginners in particular, but have selected various passively managed funds myself, whose cost structure is quite inexpensive. Every month, six different ETFs and ETCs are saved.

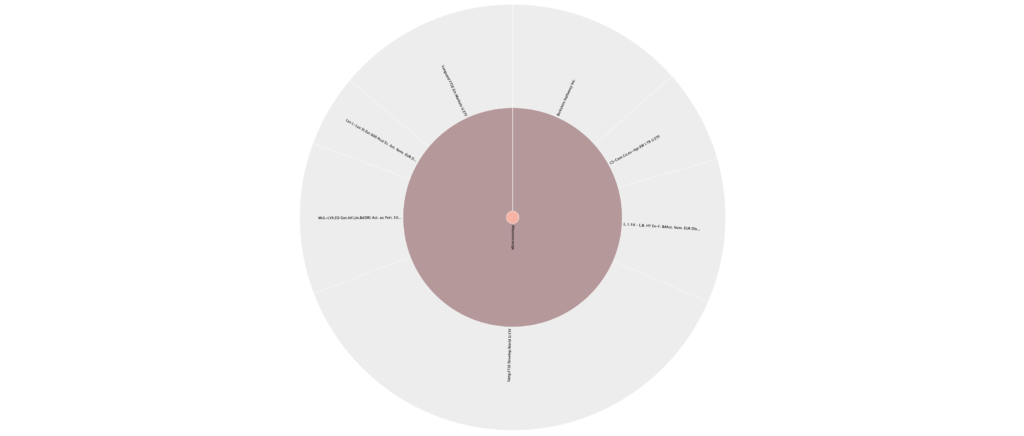

Replication of a world portfolio

With a share of 56% of the total savings amount, I put most of it into equities. 39.2% goes into the Vanguard FTSE Developed World, while 16.8% goes into the emerging markets ETF from the same provider. The composition of these two index funds is quite similar to most MSCI ETFs, but the cost structure is more interesting, with other key metrics such as fund size or tracking difference also in place. Since I rely on regular cash flow in my investing, both ETFs are distributing.

The second major asset in my fixed income strategy and world portfolio is bonds. 30% of the monthly savings amount goes into this area, and I split this position 50/50 between government and corporate shares. Specifically, this means that I put 15% of my savings rate into government bonds of developed countries and lend 15% to the largest companies.

The third and fourth pillars are 7% each in commodities and real estate, where I buy a simple ETC, or ETF, and thus diversify broadly between the respective classes.

Specifically, it looks like this:

- 39,2 % Vanguard FTSE Developed World (WKN: A12CX1)

- 16,8 % Vanguard FTSE Emerging Markets (WKN: A1JX51)

- 15 % Staatsanleihen (WKN: LYX042)

- 15 % Unternehmensleihen (WKN: LYX0YX)

- 7 % Rohstoffe (ETF090)

- 7 % Immobilien (LYX0Y0)

From time to time, I am forced to periodically adjust the positions to my desired risk. Thus, the weighting within the portfolio can shift at any time because, for example, the stock market is performing better than commodity or real estate prices. This results in shifts that have to be compensated for regularly as part of a rebalancing process. I therefore have to sell positions that are performing well and buy up positions that are performing poorly. I currently do this about every two years, which of course involves additional costs. I run the savings plans at 1.5% costs at comdirect*.